Community banks, which make up at least 90% of all banks nationwide, are the backbone of American small businesses.1 An ICBA report found that roughly 60% of small business loans and over 80% of agricultural loans come from community banks.2 But community banks face steep challenges, including net interest margin compression, compliance and cybersecurity burdens, and new, often digital-only, competitors. In fact, 93% of respondents to IntraFi’s Q1 2026 survey of bank executives say they expect deposit competition to remain at current levels or increase over the next year.

To stay competitive and continue providing the vital banking services their communities depend on, community banks need every advantage available to attract and retain high-value relationships. Reciprocal deposits are an essential tool that allow community banks to support local deposit and lending needs, enabling banks to offer large depositors access to millions in FDIC insurance while keeping funds local to lend in the community.

IntraFi is not an FDIC-insured bank, and deposit insurance covers the failure of an insured bank. A list identifying IntraFi network banks appears at https://www.intrafi.com/network-banks. Certain conditions must be satisfied for “pass-through” FDIC deposit insurance coverage to apply.

Reciprocal Deposits Typically Have a High Reinvestment Rate

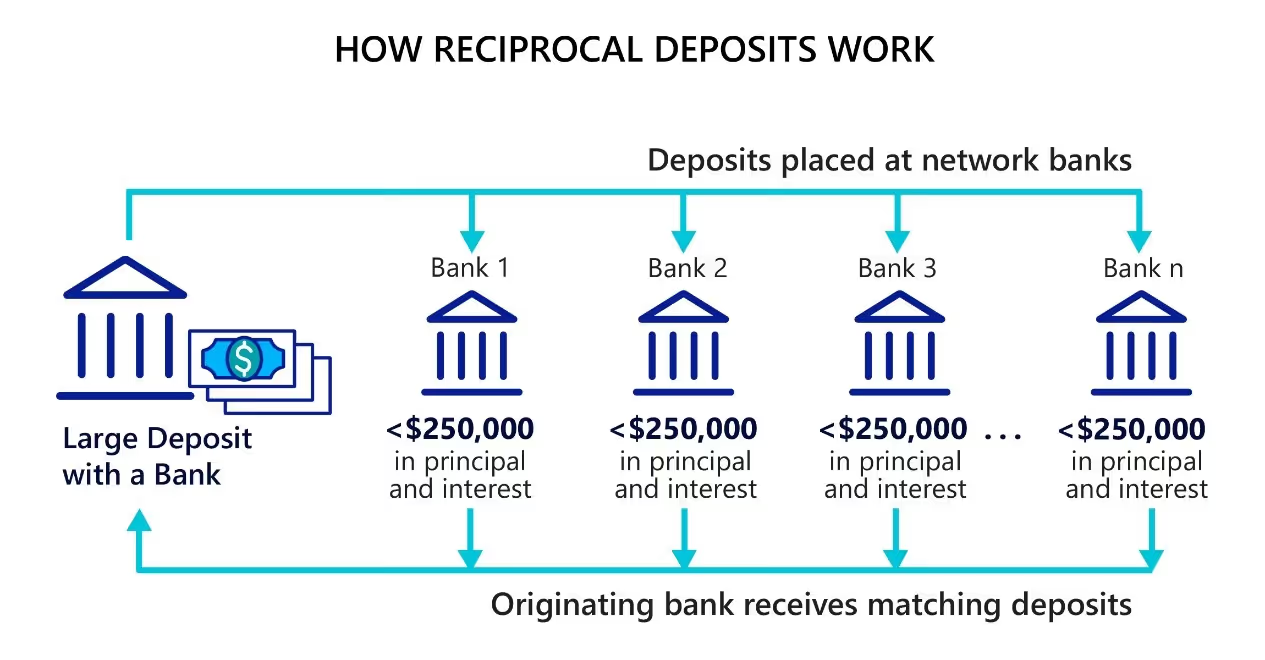

Reciprocal deposits are deposits that a bank receives through a deposit placement network in return for placing a matching amount of deposits at other network banks. Importantly, the institution placing the deposit maintains its relationship with the depositor—granting safety-conscious customers the ability to obtain FDIC insurance on large balances through multiple network banks while maintaining a single bank relationship.

At the same time, a bank that participates in a deposit placement network can attract and retain a greater amount of deposits from local customers. Historically, reciprocal deposits have been “sticky,” with high reinvestment rates and low likelihood of liquidation in any given month, even as total accounts and balances steadily increase. After the high-profile bank failures of 2023, reciprocal deposit balances at banks with between $1 billion to $100 billion in assets increased by 20% and remained elevated across 2024. A recent research paper finds that higher levels of insured deposits were associated with reduced deposit outflows during the 2023 regional banking crisis. The study also reports that banks with higher insured deposit levels paid lower interest rates on deposits, grew larger, and increased their local deposit market share over time.3 In fact, the growth rate for reciprocal deposit balances across banks of all sizes was 131% from 2022 to 2023. Reciprocal balances grew an additional 15% across 2024.4

Reciprocal Deposits Compare Well to Other Bank Funding Choices

In addition to helping banks grow wallet share from local customers, reciprocal deposits can offer several advantages when compared to other bank funding options:

• Reduced Collateralization Needs: Reciprocal deposits can reduce or eliminate collateralization requirements, freeing up pledged collateral and reducing the burdens associated with tracking collateral.

• Alternative to Wholesale Funding: Unlike many forms of wholesale funding, most reciprocal deposits can qualify as non-brokered deposits under the law.

• Superior to Listing Service Deposits: When compared to listing service deposits, reciprocal deposits can provide a more stable, relationship-based source of funding that is typically lower cost and less rate sensitive.

The Value of Balance Sheet Flexibility

Overall, using deposit placement networks provides meaningful flexibility for balance sheet management. Banks can keep funds on balance sheet as reciprocal deposits or, alternatively, sell funds into their deposit network and earn fee income (while keeping the customer relationship).5 The ability to move funds on and off balance sheet on demand can significantly reduce the need for community banks to turn away a valued depositor because of the deposit insurance limits, deepening relationships and giving banks greater control to meet their liquidity needs. Reciprocal deposits also provide a stable funding source that can be used to support lending—while providing the agility needed to respond rapidly to changing market conditions.

[1]“U.S. Community Banks: Holding up Well with Strong Asset Quality Despite CRE Exposures,” Morningstar, accessed January 12, 2026, https://dbrs.morningstar.com/research/440556

[2] “Revealed: The Impact of Credit Union Acquisitions,” ICBA, last modified December 1, 2025, https://www.icba.org/w/revealed-the-impact-of-credit-union-acquisitions

[3] Edward T. Kim, Shohini Kundu, and Amiyatosh Purnanandam,“The Economics of Market-Based Deposit Insurance, ”published September, 2024, https://www.fdic.gov/system/files/2024-09/kim-edward-paper-091124.pdf

[4] S&P Call Report Data

[5] With a depositor's consent, the bank may choose to receive fee income instead of deposits from other participating institutions. Under these circumstances, deposited funds would not be available for local lending.

Deposit placement through IntraFi Services is subject to the terms, conditions, and disclosures in applicable agreements. IntraFi is not an FDIC-insured bank, and deposit insurance covers the failure of an insured bank. A list identifying IntraFi network banks appears at https://www.intrafi.com/network-banks. Certain conditions must be satisfied for “pass-through” FDIC deposit insurance coverage to apply.